The $110 Problem Nobody's Talking About.

Earnings are exceptional, breadth is healthy, and the bull case is intact — but one variable could change everything soon.

Markets at All-Time Highs — But Not Without Caveats

Photo by Ryan Hutton on Unsplash

A strong earnings season, resilient macro data, and improving breadth paint a broadly constructive picture. Guidance trends confirm corporate confidence — but one variable is being under-appreciated by the market.

MACRO

Solid economy, sticky inflation, Fed on hold

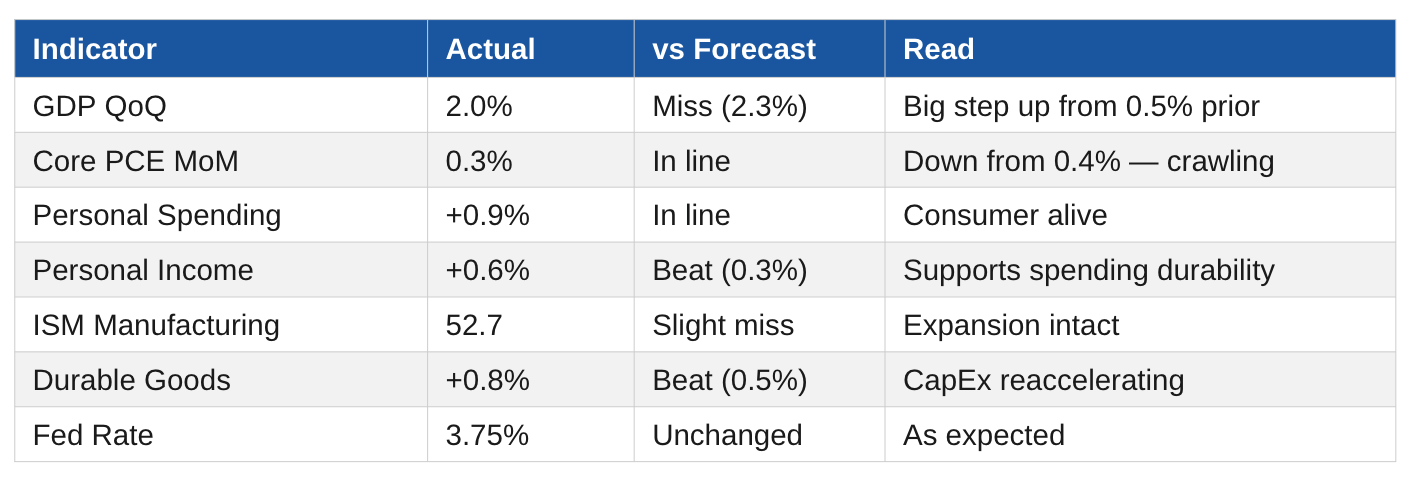

The macro backdrop holds up well. Consumer spending and income both beat expectations. GDP came in at 2.0% — below forecast, but a material step up from the 0.5% prior. Manufacturing remains in expansion, and both housing and durable goods surprised to the upside, signaling that business investment is picking back up. The Fed held at 3.75%, as expected, with little reason to move in either direction near-term.

Core PCE ticked down to 0.3% MoM — progress, but slow. And here’s the variable the market seems to be discounting: Brent crude at $110. That doesn’t show up fully in today’s PCE prints, but it will in the May and June data. If it does, the soft-landing narrative gets complicated and rate cut expectations — already limited — get pushed out further. No cuts before Q4 2026 at the earliest, and that’s optimistic. The labour market report this Friday (NFP forecast: 73K vs. 178K prior) is the next key binary event.

INDEX

S&P 500 at all-time highs on exceptional earnings

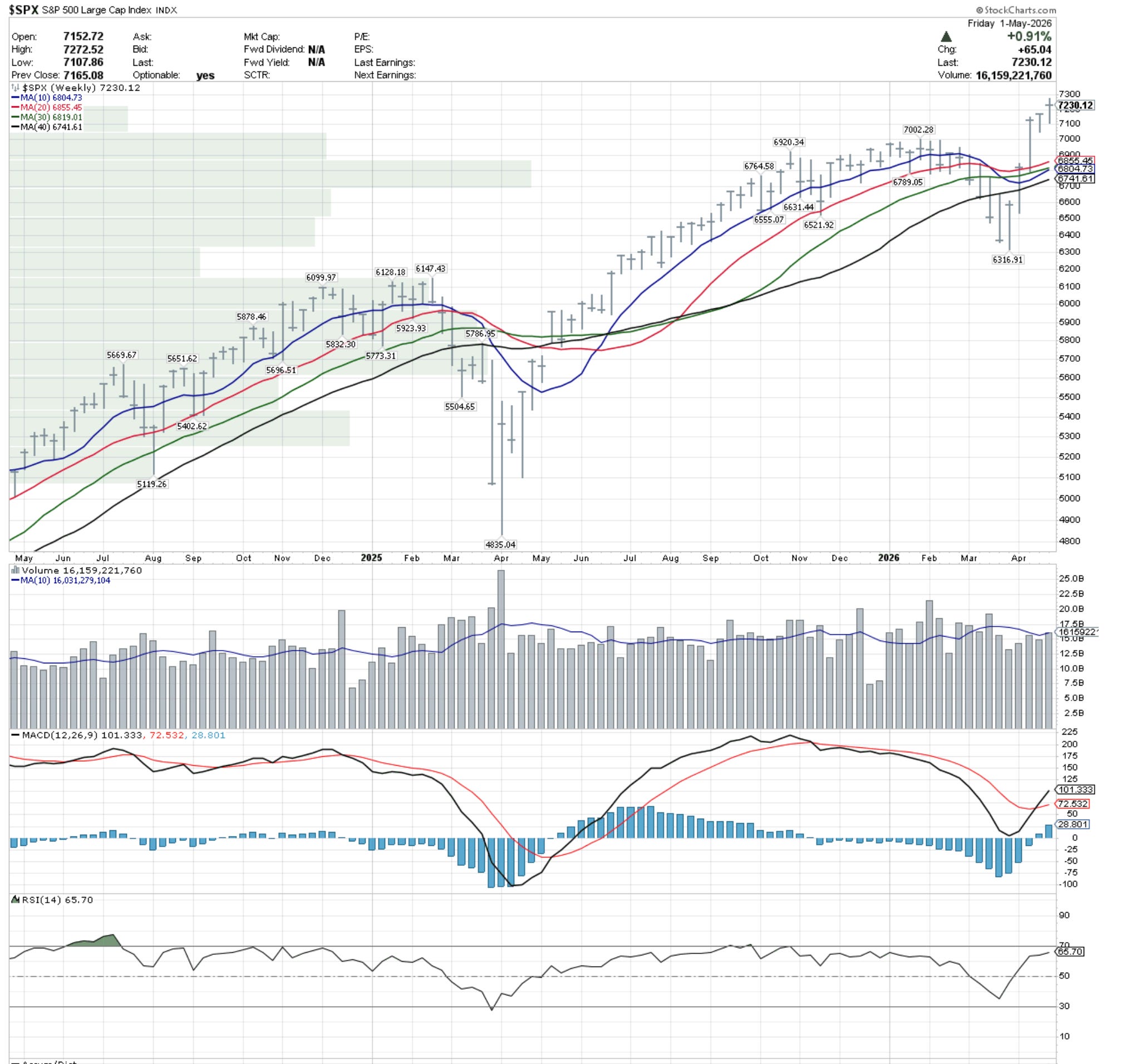

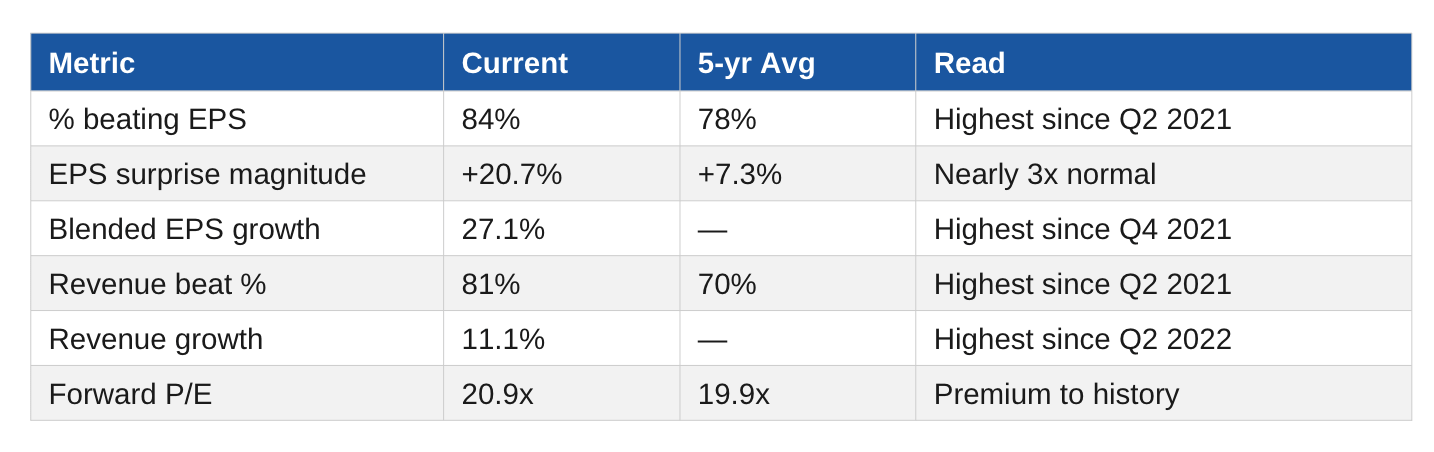

The index closed the week at 7,230 — new all-time highs, recovering from the April low in a matter of weeks. Earnings season is driving it: 84% of reporting companies beat EPS estimates (5-year avg: 78%), with a blended growth rate of 27.1% — the highest since Q4 2021. Revenue beats are equally impressive at 81%, the best since Q2 2021. Alphabet, Amazon, and Meta are doing the heavy lifting.

Technically, the picture is clean: price above all weekly moving averages, MACD bullish, RSI at 65.7. Market breadth (53.27% of stocks above their combined 50/150/200-day MAs) confirms a Positive Environment.

SECTORS & THEMES

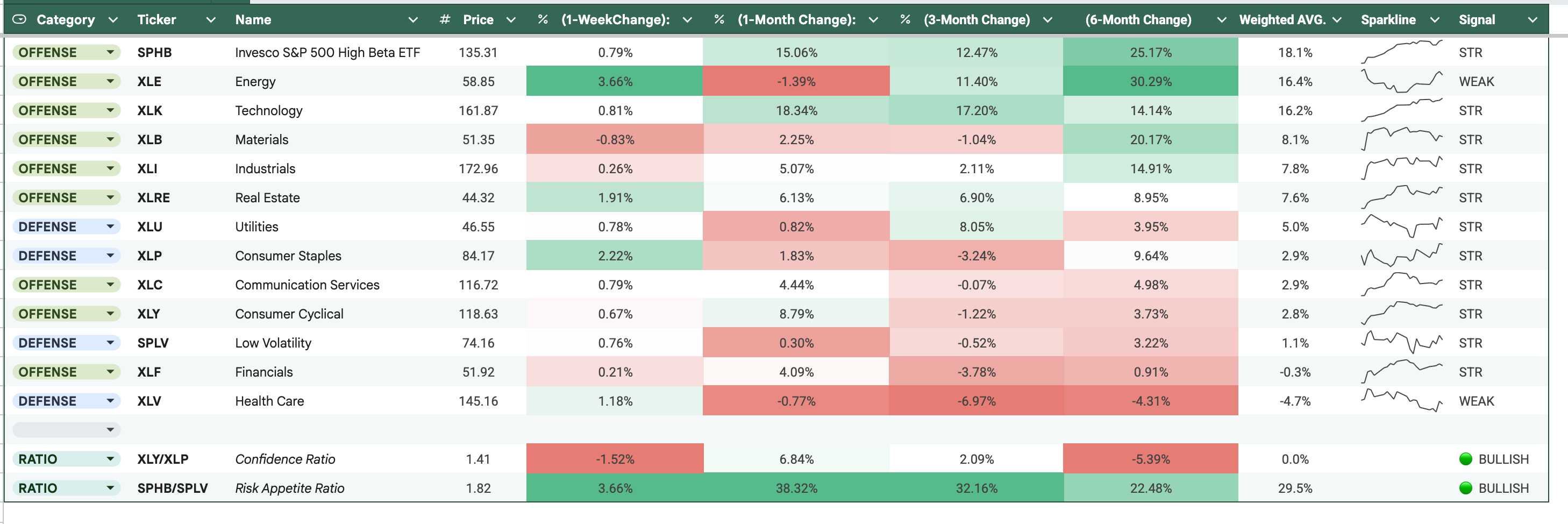

Tech and Semis lead; Healthcare the clear avoid

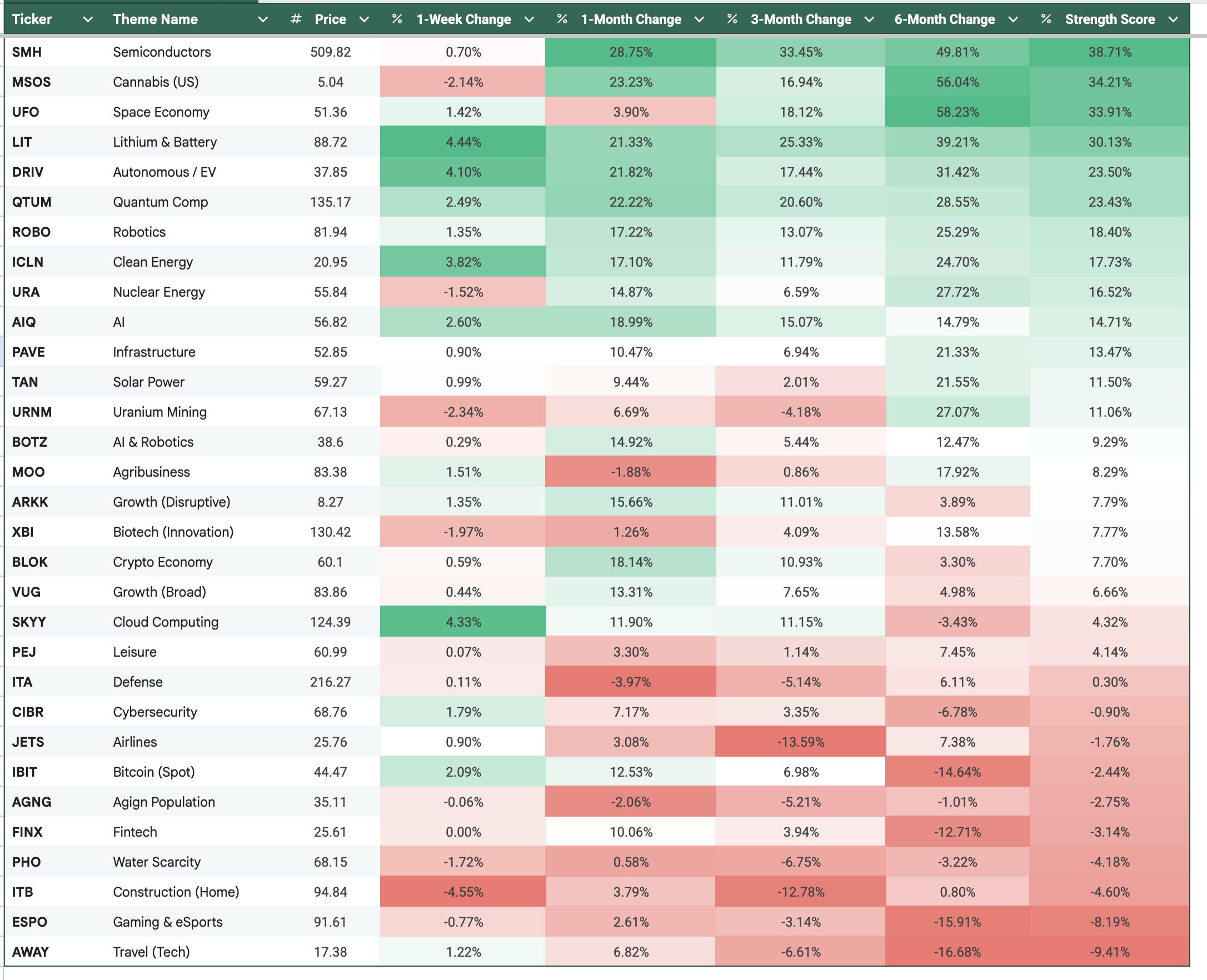

Technology (XLK: +18.34% over 1 month) is the dominant sector — directly confirmed by earnings and supported by the AI capex cycle. Communication Services is strong on earnings but more modest on price at +4.44% over the month. Semiconductors (SMH) remain the standout theme: strength score 38.71%, +33.45% over 3 months, +49.81% over 6 months — the clearest area of conviction in the current environment, by a wide margin.

Breadth across sectors is healthy: 9 of 11 sectors reporting earnings growth, 7 in double digits. The exception is Healthcare — the only sector with an EPS decline, down 6.97% over 3 months, rated Weak. No case for exposure there. Energy is the interesting one: strongest 6-month performer (+30.29%), but Weak on the 1-month at -1.39%, suggesting the $110 oil narrative was already priced in earlier. Risk appetite indicators (SPHB/SPLV ratio: +29.5%) remain bullish.

GUIDANCE

Constructive — and this matters

For Q2 2026, 28 companies have issued negative EPS guidance vs. 23 positive — a 55% negative rate. That sounds concerning, but the 5-year historical average is 58%. Companies are actually guiding less negatively than normal.

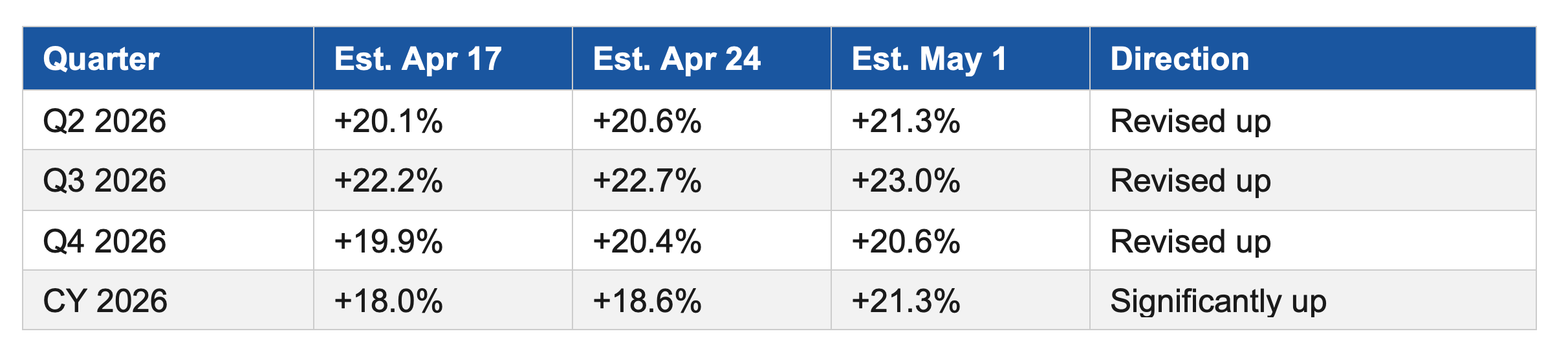

More importantly, analyst forward estimates are being revised upward across every remaining quarter — a direct reversal of the typical seasonal pattern, where estimates fall in the first month of a new quarter.

Companies are not pulling guidance or issuing widespread warnings. The Q1 beats are large enough to pull forward estimates higher — a strong fundamental signal. One caveat: the bulk of the upgrade is concentrated in Information Technology. Strip that out and the guidance picture is more modest.

BOTTOM LINE

The environment remains constructive — earnings are exceptional, guidance is improving, the macro is holding, and both trend and breadth support staying invested. The right areas to concentrate exposure are Tech and Semiconductors, where the fundamental and technical case align.

That said, this is not a moment to be aggressive at all-time highs. The P&F defensive signal, stretched valuations at 20.9x forward P/E, and the $110 oil risk to future inflation prints all argue for discipline over FOMO.

The single most important variable over the next 2–3 months isn’t anything happening right now — it’s whether Brent at $110 translates into a PCE re-acceleration in the May and June prints. If it does, the bull case gets meaningfully harder to sustain, regardless of how good Q1 earnings were.

Watch the data, not the narrative.

PORTFOLIOS

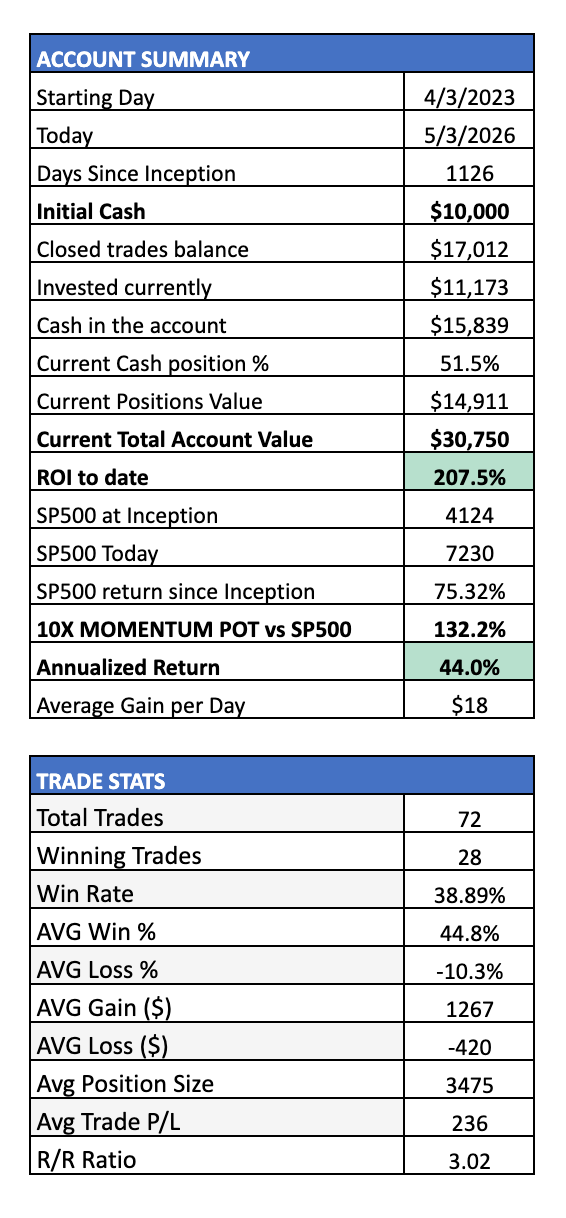

10X MOMENTUM PORTFOLIO

AMD keeps going. It's now up 64% from my entry price in under a month — a move I didn't expect to happen this fast. Extended in the short term, and a pullback is likely. I'm raising the stop loss to $290 to give it room to retrace without getting shaken out prematurely.

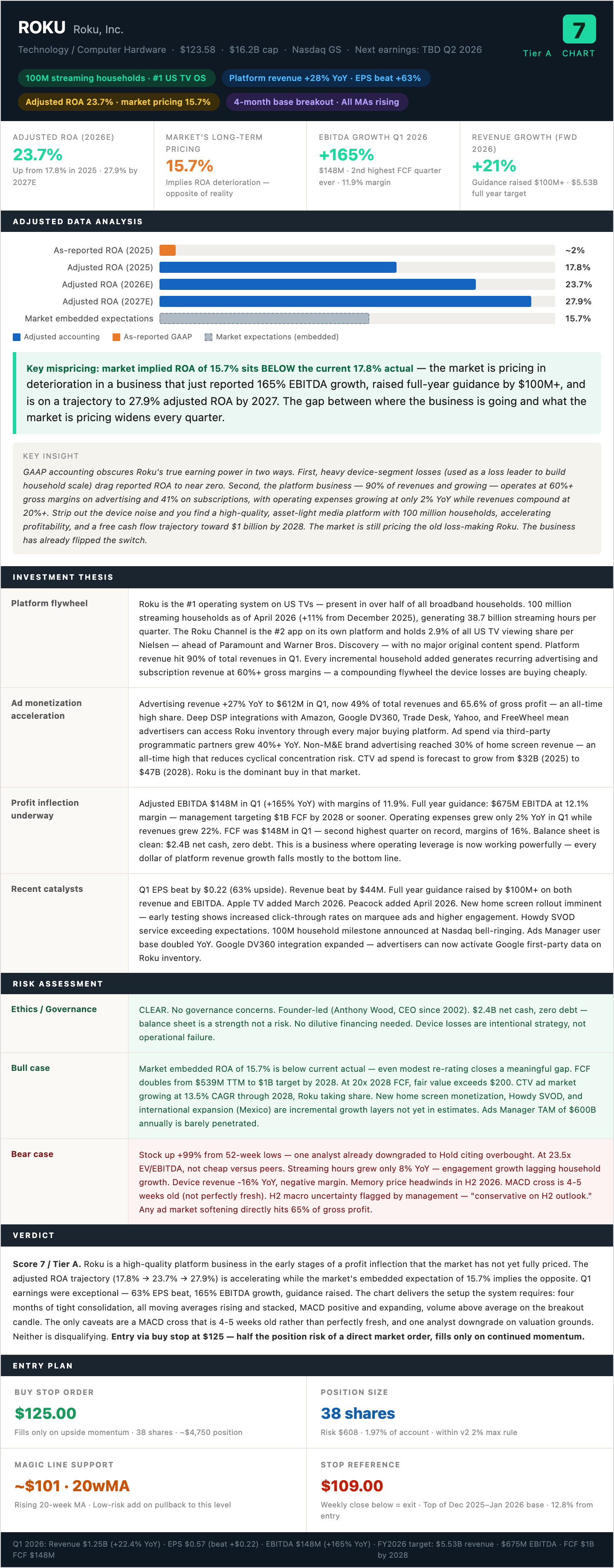

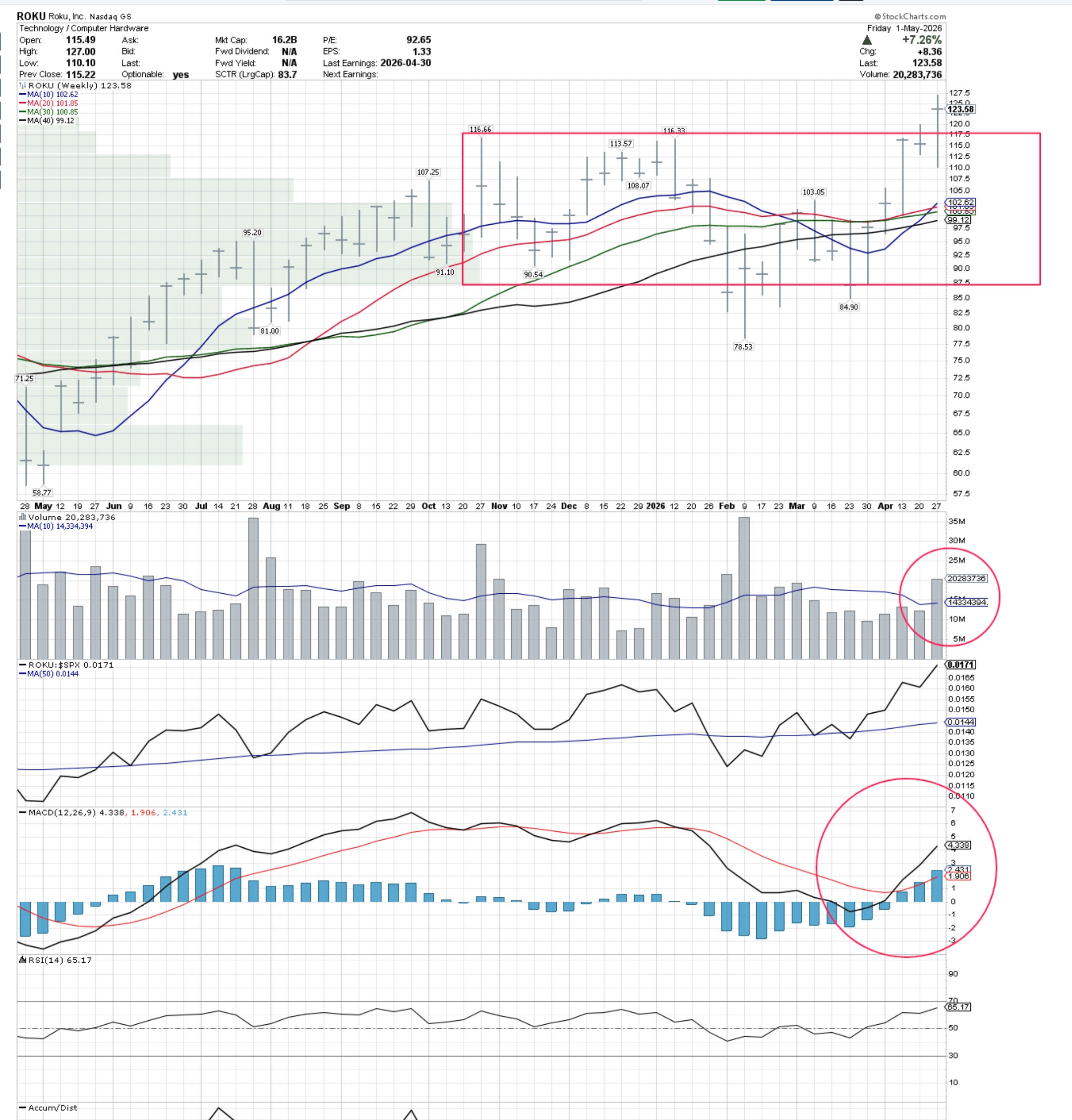

Next week I'm issuing a new BUY STOP order: 38 shares of ROKU if it touches $125. If triggered, initial stop loss at $109.

Full Thesis and weekly chart below.

Weelkly Chart

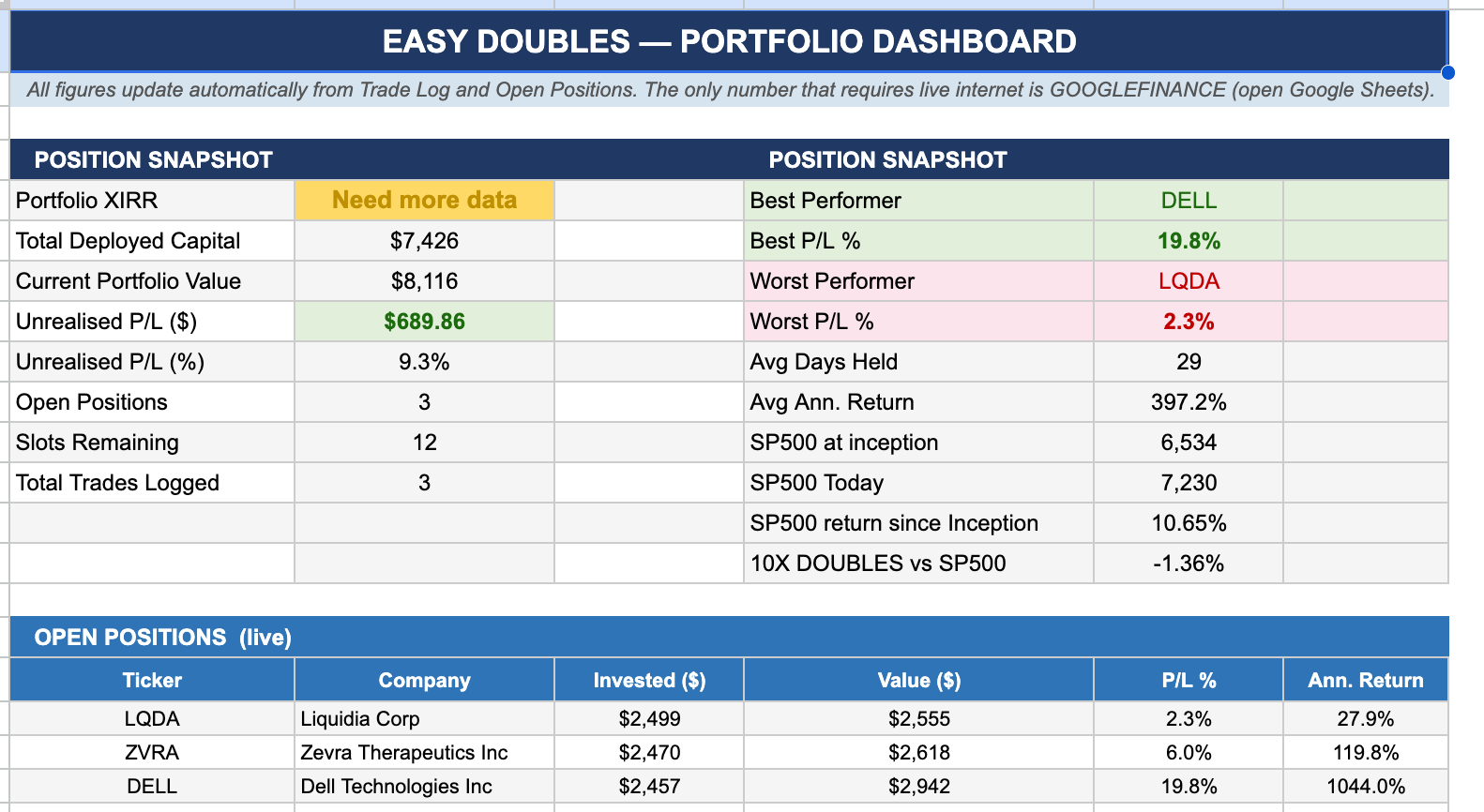

10X EASY DOUBLES PORTFOLIO

Three positions open, all in the green — a 9.3% return in under a month. This week I’m adding one new name to the portfolio.

[Paid subscribers: scorecards and current charts below]

Important: This is not investment advice. Please consult a licensed financial advisor before making any investment decisions. AI tools used for editing.